Home

Bibliography

Contact

Interesting Articles

Interesting Articles

asr5@loscostos.info

If you want your article to be published, it should the following:

- Relationship of the article with Cost Accounting

- Article source

The articles will be published only if they meet the prerequisites of quality and information.

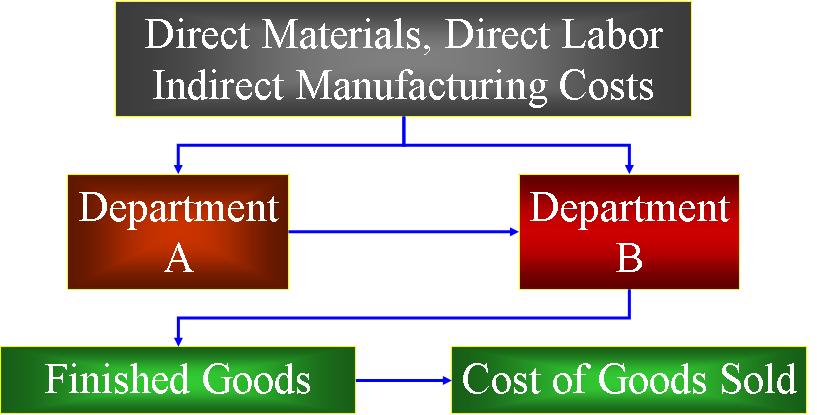

PROCESS COSTING FLOW

5 STEPS TO ACHIEVE A PROCESS COSTING

1.- Summarize the physical flow of the units to produce

2.- Calculate production in terms of equivalent units

3.- Calculate equivalent unit costs

4.- Summarize total costs to account for

5.- Assign total costs to the units already completed and to units in ending work in process inventory (WIP).

2.- Calculate production in terms of equivalent units

3.- Calculate equivalent unit costs

4.- Summarize total costs to account for

5.- Assign total costs to the units already completed and to units in ending work in process inventory (WIP).

PROCESS

COSTING EXAMPLE

Step 1. Physical units

| PRODUCTION FLOW

|

|

| Work in process, Beggining Inventory |

0

units

|

| Units started in the current period |

35.000

units

|

| Total Units |

35.000

units

|

| Completed and transferred units in the current period |

30.000

units

|

| Work in process, Ending Inventory |

5.000

units

|

| Total Units |

35.000

units

|

Step 2. Equivalent units

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

units |

|

|

|

|

Step 3. Equivalent

unit cost

|

TOTAL

PRODUCTION COSTS:

$146,050

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Step 4 and 5. SUMMARIZE

AND ASSIGN TOTAL COSTS

| TOTAL PRODUCTION COSTS: $146,050 |

||

| ASSIGNATION | ||

| Completed

and transferred units |

30,000

X $4.4014 |

$132,043 |

| Work

in process, Ending Inventory |

5,000

units |

|

| Direct

Materials |

5,000

X 2.4014 |

$12,007 |

| Conversion

costs |

1,000

X 2.0000 |

$2,000 |

| Total |

$146,050 |

|